Loss of trust

Posted 30 September 2022

This week provided the evidence for the fragility of capital markets as they grapple with the strain of transitioning from an ultra-low interest rate environment back to the one we knew before the global financial crisis of 2008. A policy mistake around the smaller part of the UK government’s fiscal measures aimed at fending off a looming recession rattled international capital markets to such an extent that it is now likely to create far more headwind than support for the UK’s economy in the winter ahead.

The media reaction to last week’s mini-budget has been deafening at times, but here at Tatton we prefer to take a step back and offer a more measured assessment of what this week’s events may mean for the UK economy and our investors.

The Chancellor’s ‘fiscal event’ came after the UK government had already announced a comprehensive support package for households and businesses to soften the blow of further energy price rises. This package is likely to cost more than three times the fiscal stimulus package through tax cuts announced by the chancellor last Friday. Markets had taken the equally debt funded energy support programme positively without any notable changes to bond yields or currency. Friday’s £47 billion economic stimulus programme, on the other hand, prompted a melt-down in the fundamentals of the UK’s capital market that was only alleviated after the Bank of England (BoE) intervened in its capacity as lender of last resort. This stabilised markets and allowed yields and sterling to recover almost back to where they had been before the fiscal event took place.

So, why the outsized reaction to the smaller programme of tax cuts versus the much more sizeable injection of public funds into the energy markets? The answer is that the former was seen as a necessary and constructive – even if fiscally painful – intervention, which would cause the UK’s economy (and thus tax revenue) to contract substantially less over the coming winter than without. But the latter, a reincarnation of a Thatcherite tax cutting strategy (but without Thatcher’s funding underpinnings), came as an utter surprise and was viewed as reckless and ineffective, because such a strategy does nothing to address the UK economy’s most pressing economic growth issues – of declining overseas trade volumes and the lack of qualified labour – while further increasing public debt levels.

What compounded the impression that lending to the UK government had just got significantly riskier was not just that those tax cuts were unfunded, but that on top the government had deemed it unnecessary to provide any detailed analysis of what this should mean for the UK’s economy, or proffered any plans on how to return to the path of fiscal prudence. This seemed like intellectual arrogance of a recent class of political actors who pride themselves in succeeding by ‘moving fast and breaking things’.

Given the UK these days relies on foreign investors rather than domestic savers to buy up newly issued government debt (gilts), and that the sterling gilt market cannot at all rely on being as big and systematically unavoidable as the US government bond market, any politician changing the perception of risk to lend to the UK government does so at their own peril – as this very young government subsequently learned very quickly.

We cover the more detailed reasons for this week’s gilt market rout in a separate article, but at the highest level, the explanation for the market turmoil is that the yield of government bonds (the ‘risk-free’ rate) constitutes the ‘plumbing’ of any nation’s financial system. It’s the pivot of the financial system with all other financial assets pricing off the risk free yield spectrum. Making this risk-free rate suddenly appear to be carrying risk therefore has very far-reaching consequences, which incidentally former chancellor and Conservative Party leadership contender Rishi Sunak unsuccessfully warned about all through summer’s election content.

The BoE’s swift and decisive action saved the government from presiding over more extensive damage in the short-term, but a fair amount of damage to the reliability of British political institutions, not to mention the damage to international trust levels, has been done. This means that the cost of capital for the UK, its businesses and consumers, is very likely to be higher than it would otherwise have been, which in turn will further reduce consumers’ ability to spend on non-essential goods and services.

And yet, despite this sobering news, it may seem surprising that in the depth of the crisis on Wednesday the UK stock market was down only around 4-5%, while the aggregate gilt market had plummeted 12-15% (by the end of this week and after the BoE intervention they were both down around 3.75%. This leads us to turn to the wider background in global financial markets and in particular the US where the wider problems for the plunging £-sterling started. The US’ somewhat different economic dynamics this year have led to a strength in the dollar we have not seen in decades, and upward interest and yield pressures that have turned monetary liquidity from abundance back to traditional scarcity.

The following excursion into how the latest developments in the US economy and financial markets have made the UK and other western nations more financially exposed takes this Tatton Weekly beyond the length of what we usually present our readers with. However, we believe the events of this week justify a deeper analysis.

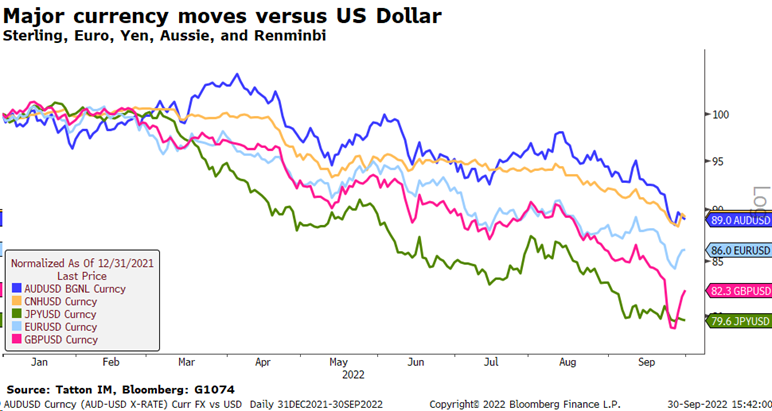

Against the relentless strength of the dollar this year (see chart below) and rates and yields higher than elsewhere, it is difficult to see how the current situation of high risks and lower returns enables Europe, UK and elsewhere to attract capital at all. The falls in the euro, Japanese yen, Chinese renminbi and sterling have been substantial.

Russia’s threat to Europe’s energy costs is keeping capital and growth flowing towards the US. But this will not go on forever and there are hopeful signs that those energy costs are starting to respond to cuts in demand and the quick reforming of distribution chains.

However, the non-US world might rather prefer if US yields started to head lower, even if that came from a soggy US equity market in response to a turn of economic fortunes across the Atlantic.

After a week of turmoil, the UK Prime Minister’s complaint that our current situation is in response to global factors is partially true. Unfortunately for her, and for her Chancellor, this was true before last week’s mini-budget. As a result of strong dollar and US yields the rest of the world could well be described as experiencing a shortage of capital. It should therefore come as no surprise that the marginal cost of asking investors for a large amount of additional funds in short order to finance increases in government debt would be much higher than immediately before. This further explains why the UK government’s blunder earned such an outsized penalty by markets this week, and why western economies are even more financially exposed to the US capital markets than usual.

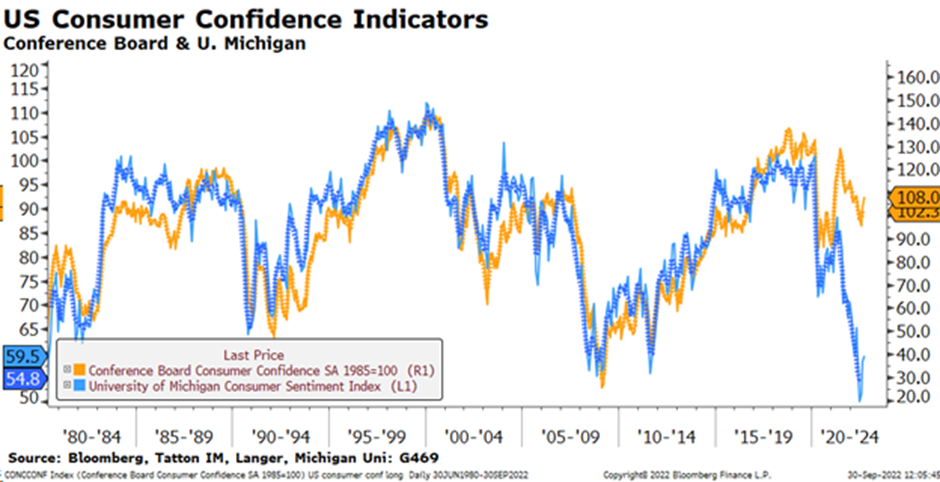

So, let us turn to the US economy to understand why yields there are so much higher as the result of resilient economic growth prospects, when the rest of the western world has entered recession. First, we have to concede that the US economy’s current insulation from the rest of the world is remarkable. The general flow of backward-looking US economic data continues to be positive despite the recent rises in interest rates. Both firms and households have regained confidence and stepped up their spending. The Conference Board’s highly respected Consumer Confidence Indicator bounced sharply as the chart below shows (orange line).

A major reason seems to be the fallback in inflation pressures from input costs, with US energy prices falling (particularly oil). Meanwhile, goods prices of imports started to decline over the summer; the strength of the dollar adding to economic weakness outside the US. The University of Michigan’s economic sentiment survey (blue line in chart above) has been weaker than the Conference Board’s indicator because it is more associated with inflation than employment. However as just about visible above, from the low, it has bounced sharply.

A fall back in input cost pressures will have been welcomed by the US Federal Reserve (Fed). Indeed, Fed Chair Jerome Powell told us as much two months ago. However, US rate setters do not see this as the inflation issue. Since August’s Jackson Hole meeting, Fed members have pointed at labour market tightness as their main concern and they have been getting more specific. In the past two weeks, various spokespeople have stated they would like to see the unemployment rate rise from the current 3.6% to 4.5%. Indeed 4.5% is their estimate of the rate which prevents this year’s price pressures turning into a self-enforcing wage-price spiral.

Returning to the Conference Board’s indicator, it is notable that it is more attuned to the labour market and therefore chimes with recent weekly employment data which confirmed there were more jobs around in September. Unsurprisingly then, wage pressure shows very little sign of subsiding. Counterintuitively perhaps, the fallback in cost-push inflation has added to growth and therefore to domestically-sourced inflation pressure. As a result, the Fed is left with little choice but to keep up the rhetoric that interest rates will have to rise and keep rising until jobs get fewer. That means for the Fed to halt tightening, firms would have to get pessimistic about revenues, not just interest rate costs.

As we head into the start of the Q3 corporate earnings season, there are some early signs of a wobble in confidence, centring on the larger more global firms with substantial non-US revenues. But, in the main, the US economy’s growth numbers tell us that well-run companies with controlled balance sheets and good cash flow will continue to be very upbeat about their prospects. They are not particularly sensitive to interest rates as refinancing is months (if not years) away. We expect their results for Q3 to look good and that they will tell us their future is positive.

Neither are US consumers particularly sensitive to interest rates. Mortgage rates have shot up to 6.7% and the housing market has slowed considerably, with new home pending sales down 20% from a year ago. But that only affects new buyers because everybody else retains the benefit of fixed rate mortgages.

As a consequence, consumer sentiment is more sensitive to the value of their saved wealth, most of which is in US equities. The renewed falls may affect confidence, much as it appeared to during the first half of 2022. The markets’ summer bounce has unwound and we are back at the lows for the year. Weak markets may mean lower consumption, which would result in lower earnings which could justify a lower market. All – admittedly – rather circular.

However, that dynamic would also enable a break in the link between bonds and markets. Markets have fallen because of interest rate-induced falls in valuation. A drop in estimated earnings for the next 12 months would allow yields to halt their previous inexorable rise, possibly even to fall.

It is perfectly possible that we could see company outlooks from this forthcoming US earnings season disappoint somewhat after all. If that is also accompanied by easing inflation pressures, we could see a reverse of the tightening of global financial conditions, something that not just central bankers across the world would find worth cheering about.

Returning to the UK, the bad start of this latest Conservative government has not improved the near-term prospects for the economy, but as laid out above, the severity of the capital market reaction wasn’t entirely free of external factors. We should be hopeful that this week’s baptism of fire will have brought home to this latest set of political leaders that the UK cannot simply apply economic textbook remedies that academics have traditionally defined under the assumption of a broadly independent economy like the US, but instead they should focus on parameters they can actually influence like trade, training of the domestic workforce, and relative attractiveness to capital and skilled labour from abroad.

After a week such as we have just been through, the domestic outlook may look particularly grim, but as the fast-moving upward developments towards the end of the week showed, the initial shock tends to be far worse than what actually happens further down the line.